JPMorgan has officially kicked off the 4th quarter when it reported earnings at 645am ET, which beat on the top and bottom line, but contained a handful of gimmicks, some weaknesses in key divisions, and as a result the stock is down about 3% in the pre-market.

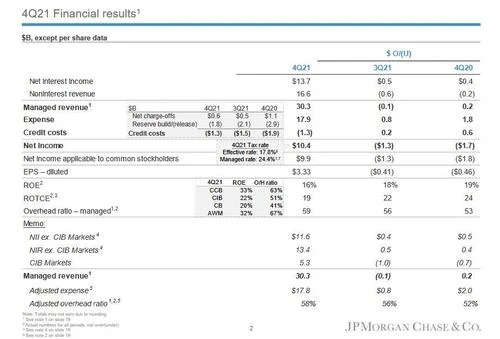

Starting at the top, the largest US commercial bank reported Q4 adjusted revenue of $30.35 billion, down modestly from Q3 2021 and up $0.2BN from a year ago, as noninterest revenue declined both sequentially and quarterly, offset by increases in net interest income. This translated into net income of $10.4BN, down $1.3BN sequentially and down $1.7BN annually, translating in $3.33 EPS, which also dropped M/M and Y/Y but beat expectations of $3.01

And while reporting another solid quarter, JPM's EPS has now declined for three consecutive quarters.

Also of note: some $1.8 billion of JPM's bottom line came from credit loss reserve releases, the bulk of which of $1.4BN was concentrated in the consumer card business. The decline in releases brought JPM's total reserves to $18.7BN, down from $20.5BN. Separately, recovery of credit losses dropped 32% Y/Y to $1.29 billion. Net charge-offs dropped by 48% to $550 million, below the estimate of $745.6 million and most of that was driven by their card business. This indicates that JPM is quite confident in the strength of the US consumer and it’ll be key to hear what they think it means about the US economy in today’s call.

Some more details from the quarter:

- Managed Net Interest Income $13.71B, Est. $13.47B

- Managed overhead ratio 59%, estimate 57.7%

- Standardized CET1 Ratio 13%, Est. 12.9%

- Return on tangible common equity 19%, estimate 17.4%

- Return on equity 16% vs. 19% y/y, estimate 13.9%

- Assets under management $3.1 trillion, estimate $3.07 trillion

Here's Jamie Dimon describing the quarter with a relatively long quarter: “JPMorgan Chase reported solid results across our businesses benefiting from elevated capital markets activity and a pick up in lending activity as firmwide average loans were up 6%. The economy continues to do quite well despite headwinds related to the Omicron variant, inflation and supply chain bottlenecks. Credit continues to be healthy with exceptionally low net charge-offs, and we remain optimistic on U.S. economic growth as business sentiment is upbeat and consumers are benefiting from job and wage growth.”

He continued:

“Global IB fees were up 37%, driven by both the Corporate & Investment Bank and Commercial Banking, due to unprecedented M&A activity, an active acquisition financing market and strong performance in IPOs. Markets revenue was down 11%, compared to a record fourth quarter last year, but up 7% versus the 2019 quarter driven by a strong performance in Equities. Asset & Wealth Management delivered robust results as we saw positive inflows into long-term products of $34 billion across all channels and regions, as well as continued strong loan growth, up 18%, primarily driven by securities-based lending. In Consumer & Community Banking, client investment assets were up 22%, with growth from higher market levels and positive net flows. Combined debit and credit card spend was up 26%, supporting accelerating Card loan growth, up 5%. Auto loans remain elevated, up 7%, although a lack of vehicle supply slowed originations to $8.5 billion, down 23%. Home lending had another strong quarter with originations at $42 billion, up 30%.”

Here, as Bloomberg notes, Dimon’s trying to warn investors that this is all slightly driven by how crazy good 2020 was for trading. In his quote, he notes that trading revenue was down in 4Q 2021 compared to 4Q 2020. But when compared to that period in 2019, revenue was actually up 7%. So last year’s trading bonanza really made for some tough comparisons this year, but based on JPM shares at the moment, that could be driving sentiment down still.

Continuing with what actually matters, we focus on the bank's corporate and investment bank, where FICC sales and trading revenue dropped 16%, and posted a surprising miss, even as equity sales and trading, investment banking, and advisory revenues all beat expectations:

- FICC sales & trading revenue $3.33 billion, -16% y/y, missing the estimate $3.42 billion

- Equities sales & trading revenue $1.95 billion, -1.8% y/y, missing the estimate $1.98 billion

- Investment banking revenue $3.21 billion, up a whopping 28% y/y, vs estimate $3.08 billion

- Advisory revenue $1.56 billion, estimate $1.32 billion

- Equity underwriting rev. $802 million, estimate $916.8 million

- Debt underwriting rev. $1.14 billion, estimate $1.03 billion

And visually:

Some commentary from the bank:

- Banking revenue was up 28% YoY to $3.2BN, with IB fees up 37% YoY, predominantly driven by higher advisory fees

- Payments revenue up 26% YoY to $1.8B, or up 7% excluding net gains on equity investments, predominantly driven by higher fees and deposits, largely offset by deposit margin compression

- Lending revenue was up 36% YoY to $263mm, driven by lower mark-to-market losses on hedges of accrual loans compared to the prior year

- Fixed Income Markets revenue of $3.3B, down 16% YoY, "driven by a challenging trading environment in Rates, as well as lower revenues in Credit and Currencies & Emerging Markets compared to a strong prior year"

- Equity Markets revenue of $2.0B, down 2% YoY, "driven by lower revenue in derivatives, largely offset by higher revenue in Prime."

And while total banking revenue rose, so did costs: expense of $5.8B, was up 18% YoY, predominantly driven by higher compensation expense, including investments, as well as higher volume-related brokerage expense and higher legal expense.

In fact, expenses overall were concerning, and in Q4, JPM's non-interest expense was $17.9 billion, up 11%. For the full year, expenses totaled $71.3 billion, which is pretty close to the $71 billion estimate that management had guided to although just slightly higher.

One wonders how much of this is due to higher compensation, and by extension will this lead to a margin compression discussion about the bankers. As Bloomberg notes, "expenses are probably going to be a huge topic today just as we work to get a sense of how the bank expects to manage its costs going forward."

Digging into JPMorgan’s asset and wealth management unit, better known as AWM, we find that net income of $1.1 billion was up 46%. Net revenue was $4.5 billion, up 16%, because of “higher management fees and growth in deposits and loans." Note that loan growth! Note also it was “partially offset by deposit margin compression.”

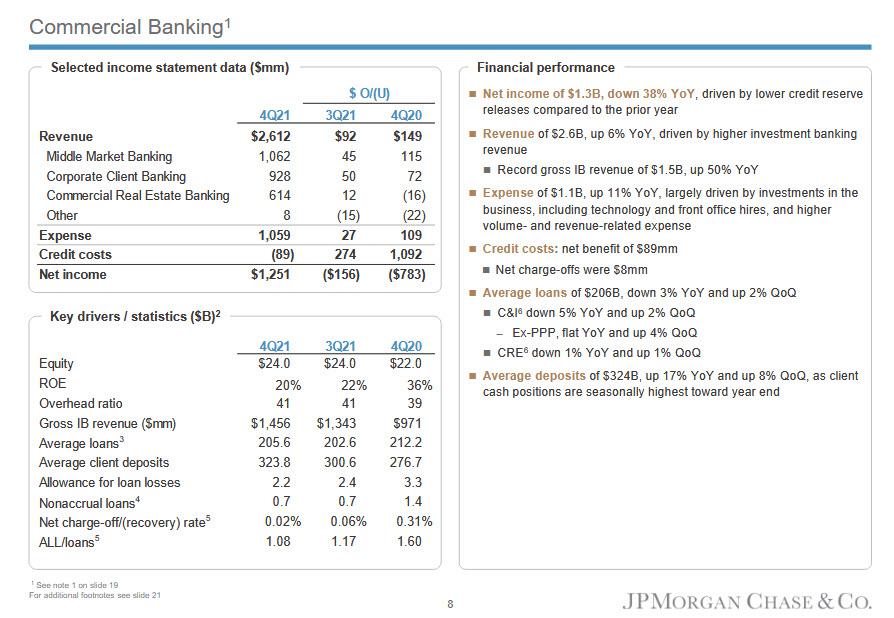

Then there is the commercial banking unit, where the highlight was that while average loans rose sequentially by a modest 2% (and were still down 3% Y/Y) to $206BN, deposits continued to surge, tracking the Fed's QE, and were up 8% Q/Q, and up 17% Y/Y to an average deposit number of $324BN. Overall, JPM reported that total loans rose to $1.08 trillion, beating the estimate $1.05 trillion; but total deposits also beat expectations printing at $2.46 trillion, above the estimate of $2.42 trillion.

{kind=link}

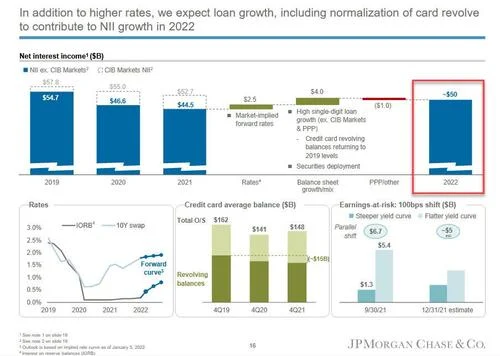

Looking ahead, the bank is guiding toward net interest income minus the NII from the markets business of $50 billion, which would be up from $44.5 billion this year. That’s from a combo of higher rates and “high single-digit loan growth” as credit card revolving balances return to 2019 levels plus some securities deployment.

While that is a solid improvement to 2021, it is well below the 2019 levels of $54.7 billion, so investors may have concerns about what is holding NII back.

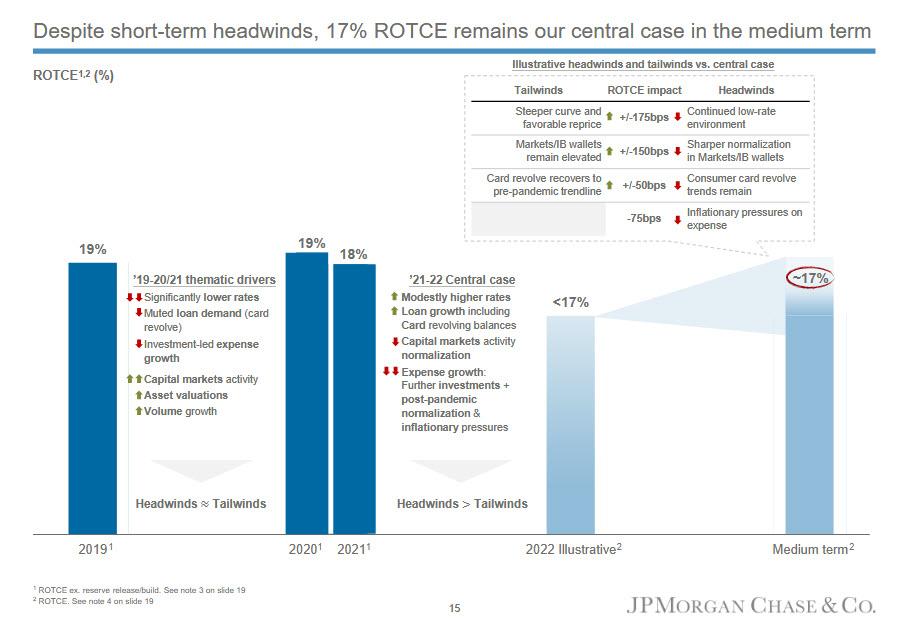

Separately, JPM still target 17% ROTCE as its “central case” in the medium term. That’s despite some short term headwinds, but includes an outlook of some modestly higher rates and loan growth coupled with more normalized capital markets activity and some expense growth.

{kind=link}

Perhaps the most interesting slide in the earnings presentation, JPM cited an adjusted noninterest expense figure of $70.9 billion for 2021 and say that should climb to $77 billion in 2022.

The biggest aspect of that increase is expected to come from investments, which could be a good thing depending on how adept you think this management team is at figuring out what businesses to deploy capital into. If not, then as Bloomberg notes, that’s a pretty solid increase in expenses. The next biggest chunk of that increase, $2.5 billion, comes from a normalization of T&E and compensation. Honestly compensation might be more of a topic than it’s really ever been for the bank just given Dimon’s comments earlier about how there’s a lot of pressure on wage growth and a huge battle over talent these days.

Commenting on this number, Bloomberg Intelligence’s senior global banks analyst Alison Williams writes that “JPMorgan’s expense guidance of $77 billion vs. $73 billion consensus may weigh on the stock, with the bank potentially to earn a bit less than its 17% medium-term ROTCE target in 2022. Higher costs to compete are weighing. Banks should and are investing in the long-term, but competition may be adding to expense levels. Expected growth in 2022 includes $3.5 billion of investment spending and a $2.5 billion increase in structural costs related to compensation and normalization of T&E.”

As noted above, expenses are “the big thing that stands out,” according to Vital Knowledge’s Adam Crisafulli, who cites higher-than-expected 4Q operating costs, and a worse-than-expected efficiency ratio, plus 2022 guidance for $77b in expenses versus Street estimates of ~$72b.

“The expense issue will be the main highlight by far for JPM (and probably the whole industry and perhaps the whole market as increased expenses/compensation is one of the tape’s largest fears).”

He also calls other aspects of the quarter mixed, with a big credit benefit --which investors will dismiss, along with soft FICC trading, solid investment banking fees, and decent loan growth.

Commenting on the earnings, Octavio Marenzi of consultancy Opimas LLC said the bank’s results “surprisingly weak,” saying they “were hampered by uncharacteristically poor expense management.” He cites an increase in non-interest expense that “looks difficult to justify.”

And judging by the stock drop in the premarket, traders agree.

Here is the full earnings presentation (pdf link here)

JPM Q4 2021 earnings presen...

(Article by Tyler Durden republished from Zerohedge.com)